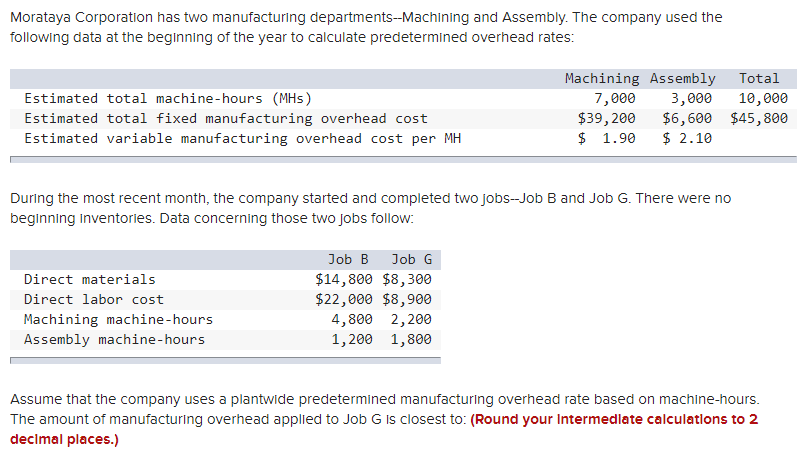

Maybe you have questioned the best way to pay for highest expenses eg property remodel or child’s college education? A lot of people have fun with a home equity financing to cover such will cost you in place of burning up the coupons.

For individuals who individual property, you could potentially be eligible for property collateral mortgage. These types of financing helps you loans things you may not be capable pick comfortably with your month-to-month income. But are there people limits in these funds? Can there be anything you can’t funds with this currency? Read on knowing just what property guarantee mortgage is and you will what you can utilize it to have.

What’s Household Collateral?

House guarantee is the difference in the brand new appraised worth of the house and exactly how far you still are obligated to pay in your mortgage and you will any property liens. Eg, say your home appraises having $two hundred,100 along with $120,100 remaining to blow in your top financial. Their remaining house collateral would-be $80,100000. You need to use a home guarantee financing to borrow against a great part of the guarantee you really have of your home.

What is actually a home Equity Loan?

The amount it’s also possible to use utilizes your guarantee in addition to house’s market price. You utilize your residence once the security into the loan, incase you have an initial financial to your family, its using to that first-mortgage. Because of this household guarantee loans usually are called next mortgage loans.

The loan will receive a-flat identity and you will interest rate, just like your first mortgage. If you get a home guarantee loan, you’re getting your money in one lump sum up front and you will always rating a fixed speed on what you obtain.

By contrast, a property collateral line of credit (HELOC) allows you to draw at stake out of borrowing from the bank since you want to buy, providing you with rotating access to bucks to have a flat mark period. Continue reading

Recent Comments